portability estate tax exemption

And as someone makes gifts during life and upon death they start to use that exemption. A surviving spouse can get a big federal estate tax break if the deceased spouse didnt use up his or her individual estate tax exemption.

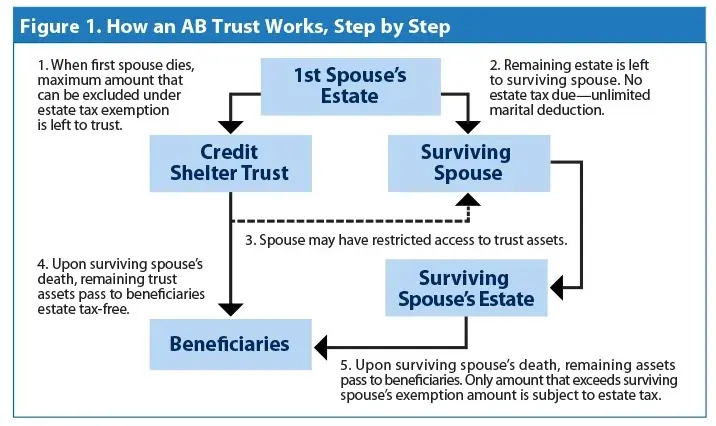

A B Trust Overview Purpose How It Works Advantages

Without portability if the first spouse died with an estate of 3000000 all of which passed to the Trust Exempt from Estate the deceased spouses unused estate tax exemption of.

. For estates that exceed this amount the top tax rate is 40. Portability allows a surviving spouse the ability to transfer the deceased spouses unused exemption amount DSUEA for estate and gifts taxes to a surviving spouse so long as the Portability election is made on a timely filed federal estate tax return IRS Form 706. Each year the government sets a tax exemption limit or exclusion amount for estates under a certain size.

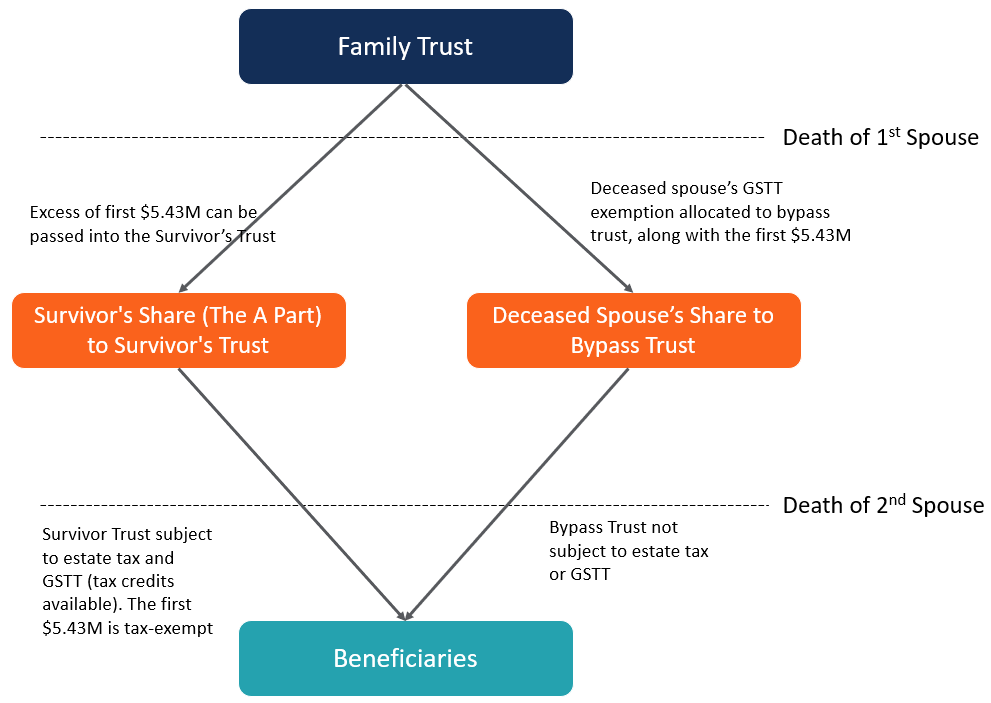

Estate tax gift tax and generation-skipping transfer GST tax. It is historically very high. The Trust Exempt from Estate Tax utilized the first spouses exemption to die and protect the assets at the surviving spouses death from estate tax.

Neither has an estate that exceeds the Federal exemption of 11580000 so no 706 is required. Currently the limit is set at 1158 million in combined assets for a decedent who dies in 2020 and is expected to remain at this level until at least 2025. This portability election increases the total exclusion.

In 2022 the estate tax exemption is 1206 million for individuals who are US citizens and 2412 million for married couples who are US citizens. Portability is the term used to describe a relatively new provision in federal estate tax law that allows a widow or widower to use any unused federal estate tax exemption of his or her deceased spouse to shelter assets from gift tax during the surviving spouses life andor estate tax at the surviving spouses death. Thanks to the portability rule the survivor can use whats left.

However by filing a 706 for portability the 5300000 unused exemption amount becomes available to the surviving spouses estate at hisher death. You will want to be aware that portability may not be the right decision for your situation if for example you choose to divide. When a tax reform measure was enacted in 2011 the estate tax exclusion became portable between spouses.

This tax has full portability for married couples meaning if the right legal steps are taken a married couple can avoid paying an estate tax on up to 2406 million after both have died. Information is still required to be provided in the return but substantially less to the extent the property passes to the survivor. Portability has been retained since then so the surviving spouse would have a total exclusion of 2316 million using the figures that are in place for 2020.

The option of portability can make a significant difference when it comes to taxation of an estate. Electing to use estate tax portability makes a significant difference in your federal estate tax liability. All that is necessary is that a timely estate tax return be filed for the deceased spouses estate.

That gives the couple a total exemption of more than. All of these taxes impact the amount of money passed to an individuals. The lifetime exemption refers to the amount the IRS allows you to exclude from your gross estate when calculating your estate tax.

There is not as much need to split the exclusions and have the estate of the first spouse to pass away get allocated into a credit shelter trust or bypass trust. In order to elect portability of the decedents unused exclusion amount deceased spousal unused exclusion DSUE amount for the benefit of the surviving spouse the estates representative must file an estate tax return Form 706 and the return must be filed timely. As a part of the resolution to the fiscal cliff the american taxpayer relief act of 2012 atra extended and made permanent a number of important tax code provisions that impact estate planning including the now-525 million estate tax exemption after inflation indexing and the portability of a deceased spouses unused exclusion amount.

This exemption means that should spouses both pass away in 2019 they have the potential ability to. But some transfers dont use any exemption. Every individual has an exemption from gift and estate tax that they can apply to transfers.

Different estate tax rules apply to non-US citizens and non-resident aliens who own assets in the United States but we are not discussing those issues here. The Tax Relief Unemployment Insurance Reauthorization and Job Creations Act of 2010 introduced for the first time the concept of portability of the federal estate tax exclusion between spouses. There are three distinct but related federal transfer taxes.

Portability in Estate Tax Exemptions. The Basics of Portability Portability essentially allows two spouses to combine their estate exclusions together into one large exemption. Estate and gift taxes are affected by the principles of portability and they are a part of a group of taxes known as federal transfer taxes.

Portability of the estate tax exemption means that if one spouse dies and does not make full use of his or her 5000000 in 2011 or 5120000 in 2012 5250000 in 2013 5340000 in 2014 and 5430000 in 2015 federal estate tax exemption then the surviving spouse can make an election to pick up the unused exemption and add it to the surviving. Currently that exemption is 117 million per person. Of the 5250000 estate tax exemption was not used by the deceased spouse can be ported to the survivor.

When enacted it was meant to apply only to estates of decedents dying before January 1 2013. The portability feature means that when one spouse dies and his or her estate value does not use up to the total available estate tax exemption the unused portion of the estate tax exemption is then added to the available estate tax exemption for the surviving spouse. Two important aspects to remember are that the portability exemption is only available to married couples and only applies to Federal estate taxes.

Portability of the estate tax exemption means that if one spouse dies and does not make full use of his or her 5000000 in 2011 or 5120000 in 2012 5250000 in 2013 5340000 in 2014 and 5430000 in 2015 federal estate tax exemption then the surviving spouse can make an election to pick up the.

What You Need To Know About The 11 Million Estate Tax Exemption Going Away

Is Ab Trust Planning Still Effective

:max_bytes(150000):strip_icc()/ScreenShot2020-02-03at1.41.37PM-322605a2b23a49598d9cdf9faee0a97a.png)

Form 706 United States Estate And Generation Skipping Transfer Tax Return Definition

Free H1z1 Keys Tickets And Br Places To Visit I Am Awesome Places To Go

Free H1z1 Keys Tickets And Br Places To Visit I Am Awesome Places To Go

A Trust May Be Taxed As Either A Grantor Trust Or A Nongrantor Trust Each Type Of Trust Has Advantages And Disadvanta Estate Tax Estate Planning Grantor Trust

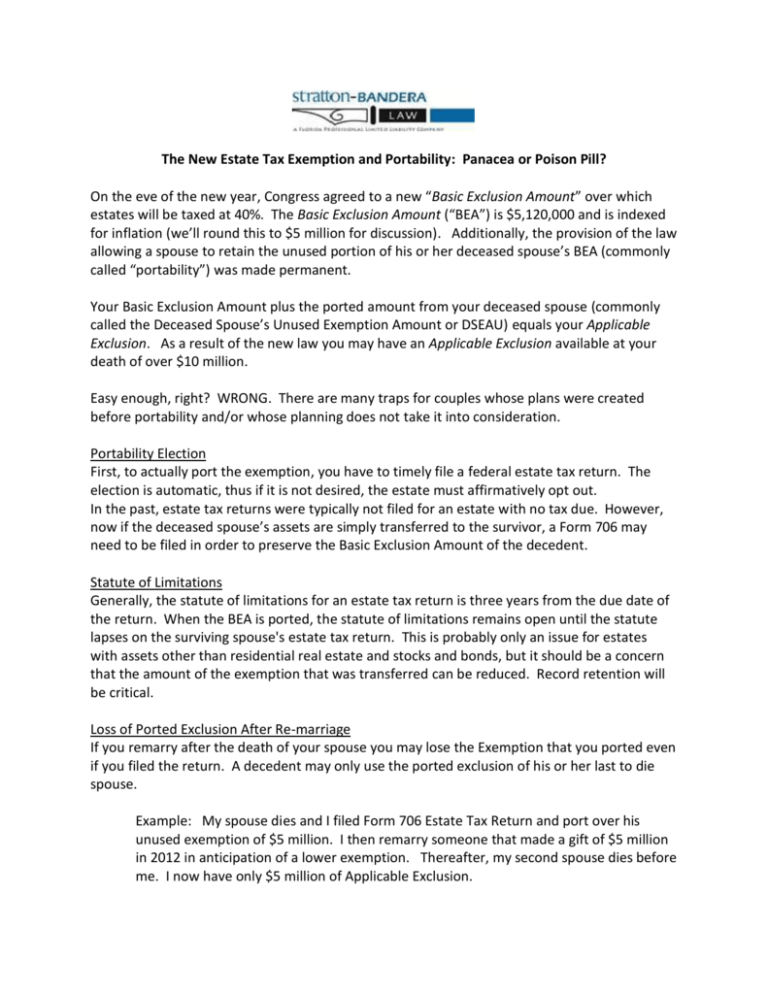

The New Estate Tax Exemption And Portability Panacea Or Poison

Pin On Estate Planning Cle

2

This Is Another In A Series Of Blogs On The Basics Of Estate Planning Estate Planning Attorneys Do Estate Planning Estate Planning Attorney Law Firm Marketing

Taxation And Initial Coin Offerings Time And Time Again I Talk To Companies That Are In The Middle Of An Ico And The Way The Initials Coins Columbia Maryland

Don T Forget About Making A Portability Election Capell Howard P C

What Is Portability For Estate And Gift Tax Portability Of The Estate Tax Exemption The American College Of Trust And Estate Counsel

A New Era In Death And Estate Taxes

Filing For Homestead Exemption In Florida Florida Homesteading Real Estate Information

Exploring The Estate Tax Part 2 Journal Of Accountancy

This First Installment Of A Two Part Article On Everything Practitioners Should Know About The Estate Tax Includes The Unified Estate T Estate Tax Home Estates

Pin By Debbie Wolfe On Trusts Revocable Trust Living Trust Estate Tax

2